The Secret Sauce to Bank Profitability

We at The Kafafian Group (TKG) have observed significant transformations in the banking landscape following the aggressive interest rate hikes that peaked in mid-2023. Our Q4 2024 Performance Measurement Peer Data reveals that the industry has now exited the six-quarter rate-lag period since reaching peak Federal Funds rates in Q2 2023, unveiling several critical shifts in profitability drivers and strategic opportunities.

Shifting Balance Sheet Dynamics

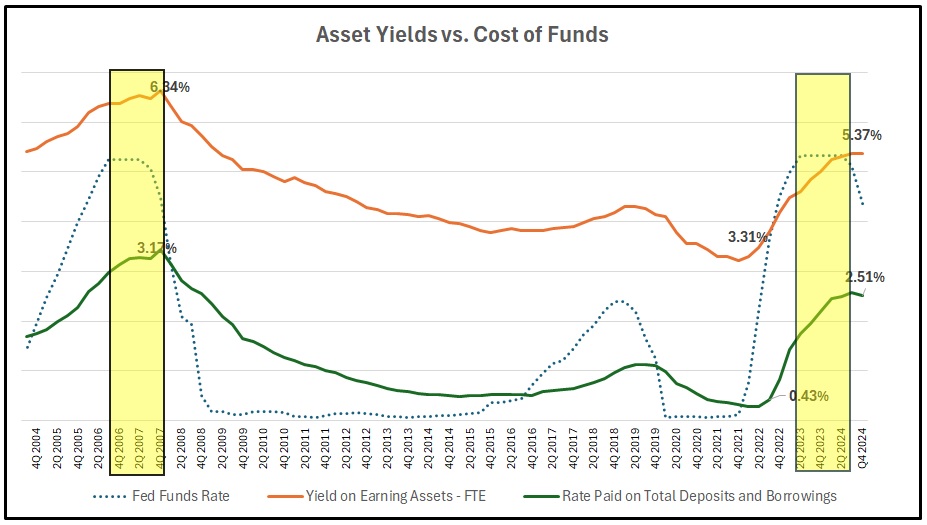

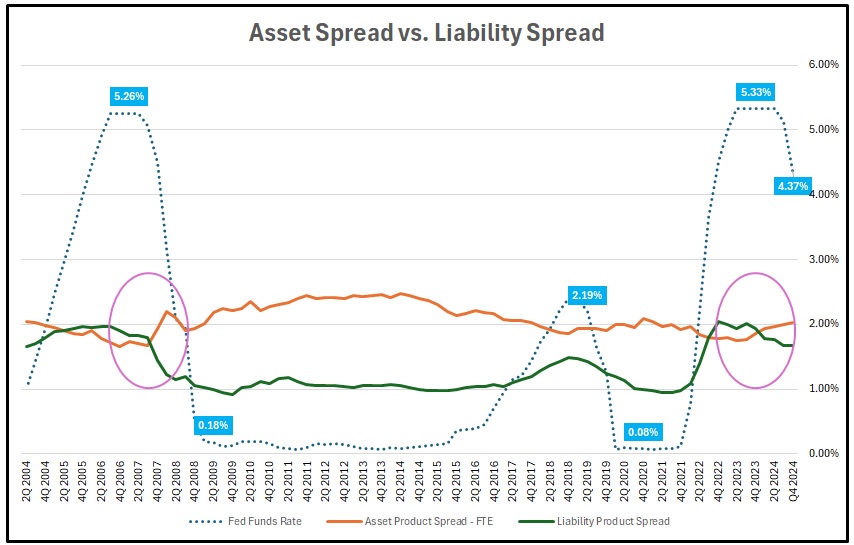

Our analysis shows that after nearly two years of challenging conditions, asset portfolios have reclaimed their position as the dominant earnings contributors on bank balance sheets from a funds transfer pricing perspective. This reversal coincides with bank cost of funds beginning to decline, creating a more favorable environment for net interest margins (NIM).

We’ve found that a flat or decreasing interest rate environment will continue to improve NIM and net spreads across the industry. However, this positive trend faces counterbalancing pressure from decreasing average deposit balances and intensifying competition for core deposits, which will inevitably drive liability spread contributions downward, potentially continuing the divergence between Net Interest Margin and Asset/Liability Spread performance.

Liability Structure Concerns

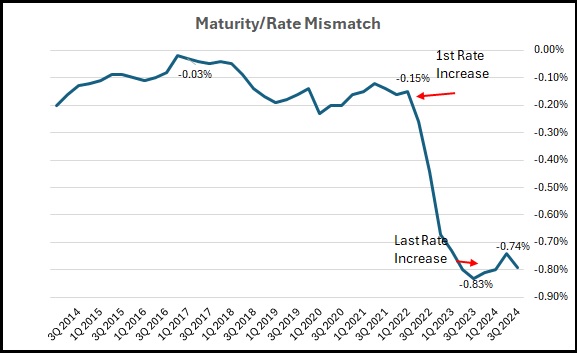

One of the most significant developments we’ve tracked over the past 24 months has been the dramatic restructuring in the duration of bank liability portfolios. Financial institutions have experienced massive certificate of deposit (CD) growth alongside increased reliance on short-term borrowings to fund loan growth. This shift to short-duration liabilities has substantially increased banks’ liability-sensitive (ALM) position, creating potential vulnerabilities if rates rise unexpectedly due to non-transitory inflationary trade policies.

We recommend two primary strategies to address this maturity mismatch: extending the term of maturing or repricing commercial real estate (CRE) loans and transitioning short-term CD balances into longer-duration money market and savings accounts. These adjustments can help institutions better balance their interest rate risk profiles and address the maturity mismatch pressure on earnings.

Unit Profitability Trends

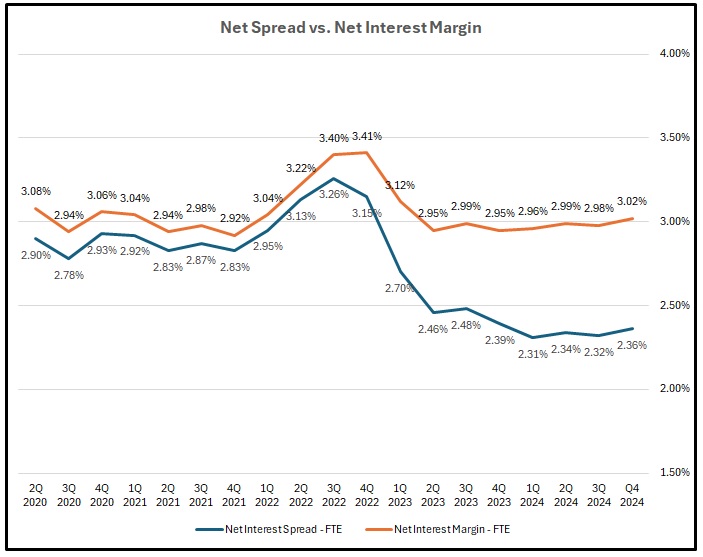

Our data indicates that branch profitability reached its apex several quarters after the conclusion of the dramatic Federal Funds rate increases. However, we’ve observed this performance metric beginning to fade as rates have remained “higher for longer” and deposit costs continued to increase six quarters after the Fed paused tightening. This trend underscores the importance of optimizing branch networks and enhancing operational efficiency.

This observation is not limited to branch operating expenses. We have observed that over half of the cost of operating a branch network comes from support functions and overhead. Realizing economies of scale means, in part, that as your bank grows, the support costs to run your branch network as a percent of the deposits in those branches should come down. It has not. And in the fourth quarter, support and overhead costs as a percentage of branch deposits stood at 1.14% of average deposits, practically unchanged since the passage of Dodd-Frank, and when the average branch deposit size was half of what it is today. Search for efficiencies there.

Conversely, we’re seeing lending profitability experiencing a resurgence as both new and existing loans are pricing at higher market levels. This development provides banks with an opportunity to rebuild margins that were compressed during the low-rate environment of previous years.

Product Profitability Analysis

Through our years of bank product analysis, we’ve identified four critical drivers of bank product profitability:

- Portfolio balance (critical mass)

- Net spread

- Average balance per account

- Expense control (efficiency)

Our research shows that commercial mortgages have reclaimed their position as the most profitable community bank product, contributing an impressive 1.91% to pre-tax return on assets (ROA). We’ve determined this product’s profitability stems from three key factors: large average balances, healthy net spreads of 2.83%, and an efficient expense ratio of 0.77%. Loan products should produce a higher ROA than deposit products because there is little credit risk in deposits. However, clients who make use of Risk Adjusted Return on Capital (RAROC) know that ROA is only half the picture. And since the Fed tightening, deposit products shine in pre-tax ROE.

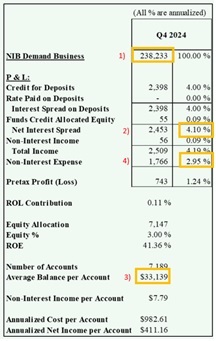

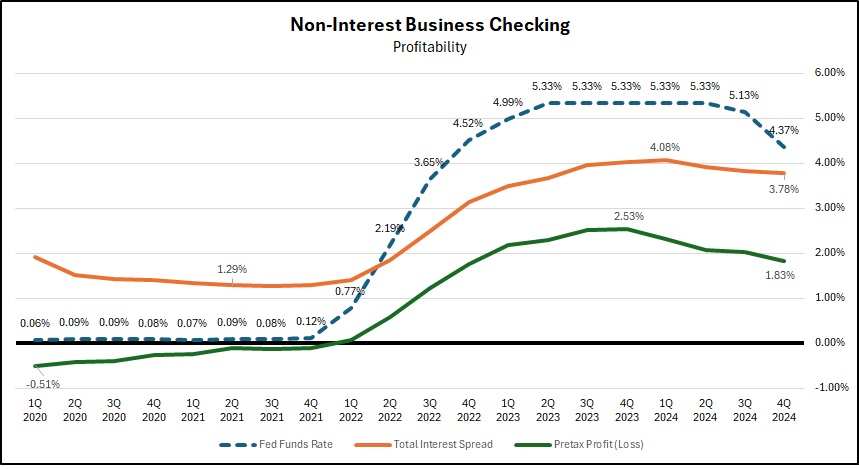

We’ve also found that non-interest business checking accounts rank as the second most profitable product in the current environment in terms of ROA. These accounts leverage a full spread of 3.78% and typically maintain substantial average balances, creating a powerful profitability engine for institutions that can effectively attract and retain business relationships. And as mentioned, the pre-tax ROE of 68.5% is, shall we say, attractive.

Strategic Recommendations for 2025

Based on our comprehensive analysis of Q4 2024 performance data, we offer five strategic insights for financial institutions in 2025:

- Deposit Strategy Refinement: We recommend institutions focus on transitioning maturing CD balances to off-rate-sheet money market or savings accounts at competitive market rates. This approach helps maintain deposits while improving the overall liability structure and creates pricing flexibility in an uncertain interest rate environment. Banks should also seek ways to build relationships with companies in their footprint that have no or little need to borrow but do have the need for treasury management services. Gone are the days when lenders can “see if the deal makes sense, then I’ll ask for the deposits.”

- Relationship Banking Focus: We continue to emphasize establishing or continuing evergreen business relationship-building campaigns. Our data clearly shows that comprehensive business relationships drive superior profitability compared to transactional banking approaches.

- Continue CRE Lending: Our analysis suggests banks should maintain a focus on doing what they do best. High credit quality owner-occupied and non-owner-occupied CRE lending is the hallmark of community banks. These are the most profitable products in the community bank portfolio. Community banks do them efficiently, and portfolios continue to perform. Just be careful not to mandate CRE lenders to be the primary deposit gatherers.

- Pricing Discipline: Refuse to fall into the trap of assuming large balances equate to greater profitability. While portfolio balance and average account balance are key contributors to product profitability, maintaining a funds transfer priced spread of 2.50% or higher is more important. We’ve consistently found that banks that have a culture of pricing discipline achieve more sustainable profitability throughout volatile rate cycles. Assign capital to products based on risk. And establish RAROC thresholds.

- Credit Quality Vigilance: Despite potential regulatory relief on the horizon, we strongly advise institutions to remain focused on credit quality. Maintaining strong underwriting standards will be essential as banks navigate economic and policy uncertainties and potential growth opportunities.

Conclusion

We at The Kafafian Group believe the banking industry stands at an inflection point as we move through 2025. The six-quarter lag effect following peak interest rates has now fully materialized, creating both challenges and opportunities. Our analysis indicates that financial institutions that can effectively manage their liability structures, optimize product offerings, and maintain disciplined pricing approaches will be best positioned to thrive.

Our data clearly shows commercial mortgages and business checking accounts represent particularly attractive focus areas, offering superior profitability metrics compared to other product categories. However, we emphasize that success will ultimately depend on holistic relationship and balance sheet management rather than isolated product strategies.

As the cost of funds begins to reverse and asset yields stabilize at higher levels, we see a window of opportunity for banks to rebuild margins and strengthen their financial foundations. Those that can simultaneously address their liability-sensitive ALM positions while capitalizing on improved lending profitability will emerge as industry leaders in the coming quarters.

The insights provided by our Q4 2024 Performance Measurement Peer Data offer a valuable roadmap for navigating these complex dynamics. By implementing the strategic recommendations we’ve outlined, financial institutions can position themselves for sustainable profitability regardless of the interest rate environment that emerges in 2025 and beyond.

For more information on our findings or to discuss how TKG can help apply them to your institution, please contact Benjamin Crowley, Managing Director, at bcrowley@kafafiangroup.com or 267.240.4920.